‘Emissions reduction’ is a phrase often thrown around despite few actually knowing of the layers of complexity behind its execution. There is no cure-all strategy for the abatement of carbon emissions, simply because emissions arise at every stage of the oil and gas value chain, each stage requiring its own specialised treatment strategy. In order to tackle emissions in a comprehensive manner, one must first understand the nuances behind their origins.

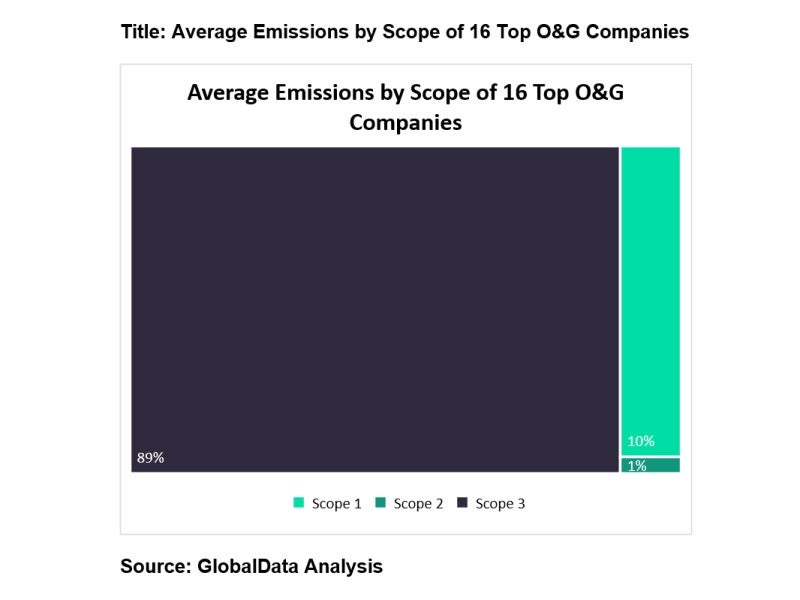

Scope 1 and 2 emissions add up to about 10% of total emissions from oil and gas companies, with the remainder being accounted for by Scope 3. This disparity fails to explain why Scope 3 emissions are so often left on the backburner when companies draft up their emission reduction strategies. To illustrate this point, of the 28 major oil and gas companies, 96% have plans to reduce Scope 1 and 2 emissions while only 43% are attempting to target Scope 3, based on GlobalData’s latest report on Emission Reduction Strategies. It isn’t just a case of companies ‘slacking off’, but rather the fact that Scope 3 emissions are notoriously difficult to measure. It is when products are sold and passed on to consumers or third parties that things get very hazy, very quickly, as a result of other factors coming into play, such as consumer habits and potential miscounting of emissions due to poorly defined scopes.

Go deeper with GlobalData

Strict targets spark innovation

Of Scope 1 and 2 emissions, the most potent contributors come equally from upstream and downstream activities. Corporations have risen to the challenge of addressing these emissions through the deployment of low-carbon emission fuels, carbon capture technology, hydrogen-based projects, as well as the electrification of operations.

Increased societal and political pressure has forced companies to put their thinking caps on and come up with innovative solutions to achieve progressively harsher targets. Equinor, for example, has plans to power its upstream operations with floating wind technology upon the establishment of its 88MW Hywind floating wind project. Likely the first of its kind to power offshore oil and gas facilities, this project will provide an estimated 35% of the annual power demand in the Snorre and Gullfaks fields. With regards to downstream facilities, Shell, Eni and Repsol have invested heavily in developing biofuels and constructing biorefineries, with the latter co-heading a pilot project for an e-fuel production plant in Bilbao, Spain.

Divestment of thermal assets, mainly those past their prime, has been adopted as a strategy to curb emissions across all scopes. At first glance, this may seem like a lost cause as it does little (if anything) to reduce the global contribution, merely offloading emissions onto a different operator. However, it can be seen as a company’s means of starting with a clean slate, funnelling its divestment proceeds into low-carbon businesses and expediting the development of renewables. BP is banking on its divestments to reduce future demand for fossil fuels.

Placing a price tag on carbon

Most of the Western oil and gas producing nations have plans of committing to net zero carbon emissions by 2050. Ambitious goals such as these warrant the implementation of an effective mechanism to hold companies accountable and, in recent years, carbon pricing was thought to be the way to go. Carbon pricing on a nationwide scale translates itself into two forms, for instance, carbon tax and an emissions trading system (ETS). Countries such as Canada, Mexico, Norway and Finland have adopted both forms of carbon pricing while others have stuck to a single mechanism – namely China and Germany with ETS, as well as Argentina with its carbon tax. For other developing nations, emissions reduction remains at the bottom of their agenda as their attention lingers on progressing the economy and providing energy accessibility to citizens.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataA carbon tax places a fixed fee on greenhouse gas (GHG) emissions, creating certainty surrounding carbon prices. An ETS, on the other hand, is a market for trading carbon allowances whereby the price of carbon is dependent on the market value, creating instead a certainty in overall emissions reduced. As allowances become fewer in number, the resulting scarcity leads to a hike in prices, making it cheaper to just invest in low-carbon technology. Purchasing allowances is after all simply a means of delaying the inevitable. Reluctant to succumb to the unpredictable nature of the ETS market, many US oil and gas companies are in support of carbon tax as a way of levelling the playing field.

In regions where such initiatives are less commonplace, corporations have taken to imposing an internal carbon price, in the expectation of a future carbon pricing scheme. GlobalData reports that BP is imposing a carbon price of $100/ton by 2030 on projects exceeding a fixed GHG emission threshold while Chevron accounts for elevated prices of $250/ton in advanced economies in 2050.

While the effectiveness of carbon pricing schemes is still up for debate, our best bet right now is to make use of all the tools at our disposal, in hopes that a multi-pronged attack is sufficient to bring about meaningful change.